Jardine Matheson: Possibly Too Extreme A Case Of ‘China Discount’ (OTCMKTS:JMHLY)

Architectural Visualization

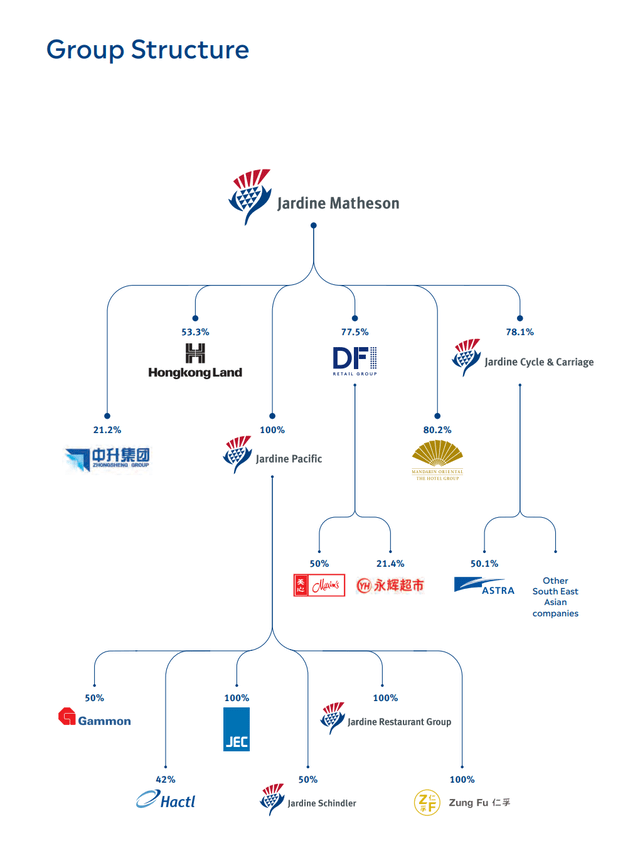

Jardine Matheson Holdings Limited (OTCPK:JMHLY, OTCPK:JARLF) (we’ll call it JM or just Jardine for short), together with its listed subsidiary Jardine Cycle & Carriage Limited (OTCPK:JCYCF) (C&C for short), represent major businesses in Hong Kong and China’s mainland. Together, they have characteristics that would typically invite a high multiple: clear tangible value, profit growth thanks to the end of COVID-zero, relative resilience and track record. Indeed, Jardine Matheson, a storied conglomerate with a long history in Hong Kong, just a few years ago used to command quite a premium valuation.

Now, however, JM’s comprehensive P/B has plummeted, and the valuation of assets outside its well-performing Indonesian and SE Asian businesses in C&C has plummeted even further than that. We think there is an angle where allocators become comfortable again with Chinese allocations, with JM being a very operationally solid pick with massive amounts of value to gain on it returning to its more premium status.

On the other hand, we have been bearish on China for years over the foundational issue of how secure Chinese securities actually are, and how that concern articulates with geopolitical conflict. We see it as a very compelling headline income and value play, but recognize the risks and will never go beyond a very speculative allocation to the stock.

Earnings FY

Since this is our first coverage, we want to be comprehensive, also for our own reference in the future, and look at performance segment by segment, since its presence is quite sprawling.

Structure (AR 2023)

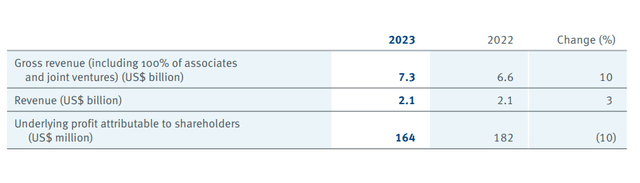

Jardine Pacific (9% of underlying operating profits)

Jardine Pacific is composed of several businesses. These include a couple of heavy engineering businesses (Gammon and JEC). Another is Hactl, which is a major warehouse where cargo from air freight is handled in Hong Kong; this is apparently the world’s largest of such facilities. Then there is the Schindler (OTC:SHLRF) and Jardine joint venture that is focused on escalators, elevators, etc., for the Asian markets ex-China. Also, a restaurant group, which is a major franchisee of Yum! (YUM) focused on the major Southeast Asian markets, and finally Zung Fu, which is an automotive group, operating as an exclusive Mercedes-Benz (OTCPK:MBGAF) retailer (both commercial and passenger vehicles).

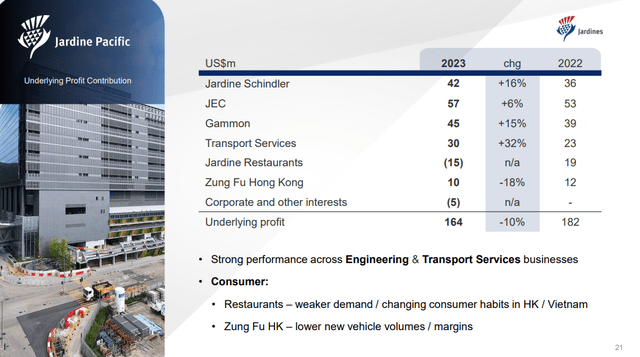

Jardine Pacific Highlights (AR 2023)

Profits declined around 10%, but would have risen absent the government subsidies supporting profits in 2022 of $28 million.

Jardine Pacific Businesses (FY Pres)

Jardine Schindler performed well, with higher sales in line with performance expected of its razor-and-blades business model. New installation was unsurprisingly weak, with the region’s China-connected economies struggling a bit, but maintenance did well.

Gammon had higher sales, but projects phasing and timings hit margins. They still contributed to growth, YoY. Operational improvement programs have been helping. Even JEC had decent performances YoY. Much like the end of the subsidies coincided with the end of COVID-zero in China, some of this recovery owes to a bit of a resumption in these economies, although concerns around the Chinese property markets remain high.

Zung Fu reported lower profits despite stronger after-sales performance, which tends to be a higher margin business. There were volume issues here, also due to supply chain impacts from Hyundai. But generally weak consumer sentiment is a factor, particularly in Hong Kong end markets, in which Zung Fu is focused. Jardine Restaurants didn’t do well, coming in at a net loss. Low-ish traffic at the same time as lacking government subsidies are a problem here for now. Apparently, quite a lot of outbound traffic from HK these days is to Shenzhen.

Jardine Pacific is around 5% of revenues and around 9% of underlying profits.

Operating Profit Breakdown (FY Pres)

Astra (44% of underlying operating profits)

Astra, main C&C business (FY Pres)

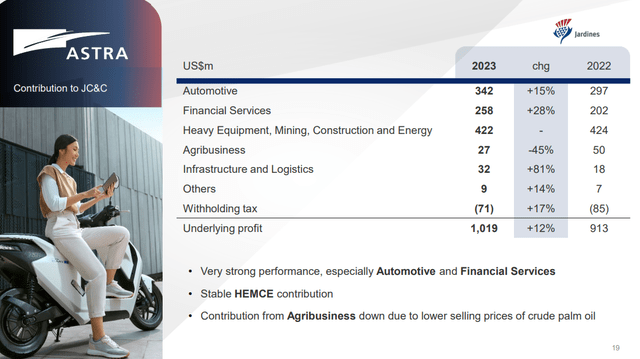

The major businesses in Astra are automotive, financial services and heavy industry including mining and energy. There was modest growth in underlying profits. These businesses are focused primarily on Indonesia, and there isn’t really any Chinese exposure.

The automotive business assembles and distributes certain Japanese and French car brands for the Southeast Asian market. Motorcycle sales rose considerably, while car sales shrunk slightly, but the net effects, thanks to the prevalence of two-wheeled vehicles in Southeast Asia, were very positive. The 80% owned auto parts business also grew due to major margin gains on pricing hikes for auto parts.

Financial services saw considerable increase in net income thanks to its growing consumer finance businesses at 15%. Heavy equipment financing also grew 8%. The insurance business also grew due to growth in policies underwritten.

For the heavy industries, they have their United Tractors business which bought a stake in a nickel mine, even though nickel has been going down on over-mining, particularly in Indonesia. United tractors overall saw stable performance thanks to aftermarket sales offsetting new equipment declines. Their contract mining businesses are doing decent, as well as their construction machinery business, offsetting some of the pressure in coal mining and also the effects of a lower rate of gold mining. The overall segment is running stably and has flat operating profit evolutions.

Palm oil price pressure hit the agribusiness, while net income almost doubled for infrastructure and logistics, primarily due to their toll road and logistics businesses. They have the concession for some roads in Java and the outer Jakarta ring road. It’s a small contribution, though.

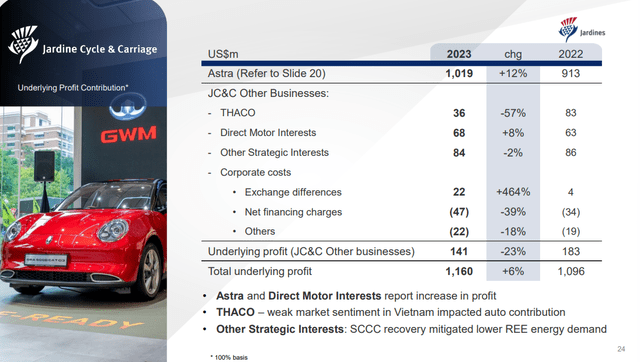

Jardine Cycle & Carriage (6% of underlying operating profits ex-Astra)

C&C ex-Astra (FY Pres)

Astra is technically within this segment, which is also a publicly listed company in its own right, with close to 90% ownership by Jardine Matheson. But here we focus on the ex-Astra businesses. The residual operating profit of businesses outside of Astra is small, at around $40 million only.

Direct Motor Interests, which include the Myanmar, Singapore and Bintang businesses as well as Tunas Ridean. Most of these are car distributing businesses. THACO is a Vietnamese automotive manufacturing business. Pressures on the Vietnamese economy made problems here, with income halving. The remaining businesses were relatively stable, involved in dairy production, cement manufacturing and engineering. The generally strong end markets in Indonesia and Southeast Asian infrastructure development kept things flat here.

Hongkong Land (22% of underlying operating profits)

HKL (FY Pres)

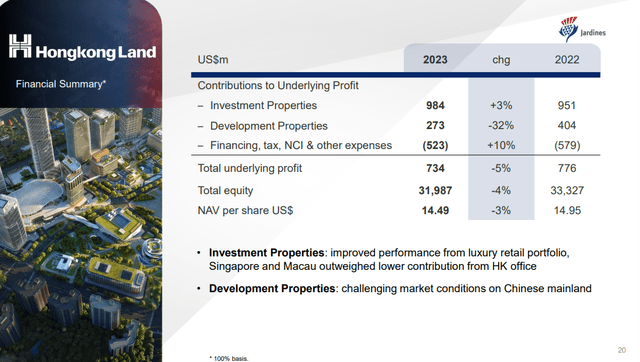

The Chinese mainland is where unsurprisingly the company saw challenges in developing properties with offsets in a strong Singaporean market, even though the income properties continued to perform well with modest growth. Underlying profit shrunk by 5% when excluding some portfolio re-evaluation effects. The bottom line is that development suffered on worse mainland property prices, which is where the developments were mostly happening. HK property markets are also struggling, but it seems this is not where the company had been making its investments.

There were some pressures in the investment property segment from HK offices, which while sporting vacancy rates that are a lot lower than in the West where work from home has taken more hold, has seen some rising. Singapore offices did fine, and the overall growth is from a recovery in retail and luxury properties driven by the return to normal following the COVID-19 restrictions in 2022, which made for an easy comp.

The development business had some residential assets in Wuhan that didn’t perform, and the general deleveraging going on in the Chinese economy is the other concern that likely keeps a lid on this segment’s results for a while longer. However, interest in contracted sales, the metrics to follow the sales of developed properties, is a little bit on the up.

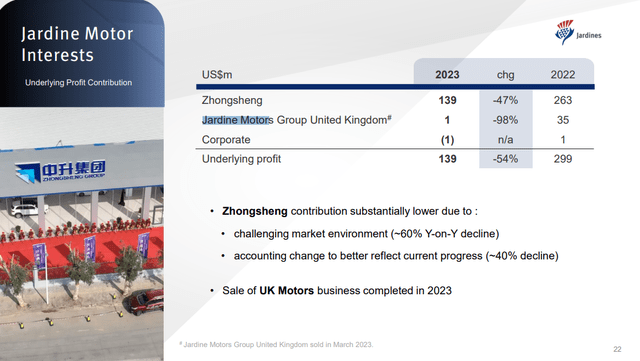

Jardine Motor Interests (8% of underlying operating profits)

Motor Interests is a similarly sized business to Pacific. Around 40% of the decline is due to accounting changes in Zhongsheng (OTCPK:ZSHGY) (publicly listed, in which Jardine Matheson has a 21% stake). But the market environment has also been challenging due to the EV shift and general pressure on consumer sentiment. Zhongsheng is a dealership business focused on the usual suspects of premium brands, all of which haven’t made a meaningful EV shift. The UK business was sold completely early in 2023.

JMI (FY Pres)

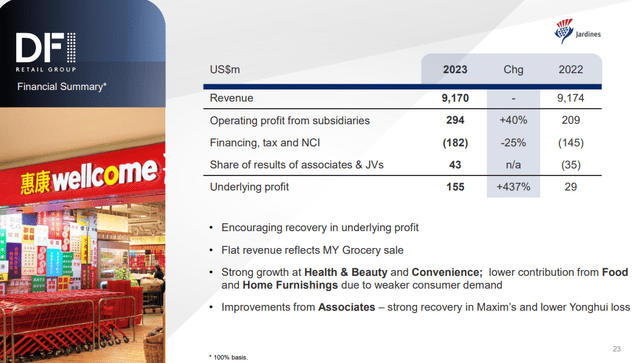

DFI Retail Group (7% of underlying operating profit)

Breakdown of DFI (AR 2023)

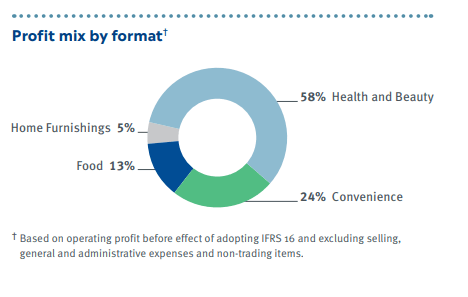

Performance was almost entirely driven by improved operational profitability. In the Food segment within the retail group, revenues were down around 5% excluding the effects from a divestment of a Malaysian business. The issue was tougher comps from pantry stocking behavior in 2022 due to pandemic-era behavior. In Southeast Asia, there was general pressure from higher costs of living and general economic pressures. Underlying operating profit fell by around 50%.

In Convenience sales grew by 8%, mainly driven by the first half of the year when the second half was more flat due to the amount of outbound travel from Hong Kong, particularly during weekends. A strategic focus to move away from taxed sales of cigarettes and into other products also lifted margins. DFI has the 7-Eleven brand for use in Chinese markets and Singapore. In general, there are usually more levers to pull for performance in convenience, as there is more pricing power and the stock tends to be higher margin. But the general reopening and increased foot traffic in key markets has been critical. Operating profit for the Convenience segment is up 74%.

Health and Beauty grew by 20% like-for-like thanks to Mannings in particular, and the general profile of the Health and Beauty retail model which relies on foot traffic that has recovered. Operational improvements were also important for driving an overall 127% increase in underlying operating profit.

Home Furnishings suffered a bit on the weakening property market sentiment, falling 7% on an LFL basis in terms of sales. Underlying operating profit here dropped by about a third. Doesn’t matter too much as this is a small element of the DFI retail mix.

DFI Headlines (FY Pres)

The Associates segment is ownerships in various other businesses like Maxim’s focused on restaurant activity in China and other parts of Southeast Asia which had a strong recovery due to the end of COVID-zero and the return to dining out. Yonghui is a supermarket group, where losses thinned thanks to operational improvement but were still challenged by local competition, which isn’t very bullish. Robinsons Retail Holdings, which is a Philippines retailing business, primarily focused on groceries, has been doing well operationally with strong sales and operating profit growth, but the associate contribution has been poor due to FX and also due to higher interest costs.

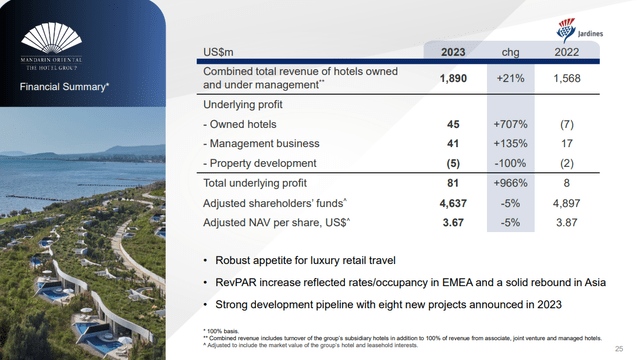

Mandarin Oriental (4% of underlying operating profit)

Headline Results (FY Pres)

Here, the reopening of the markets caused a massive reversal in operating profits that had been negative or close to negative for some years. Two new hotels were opened in 2023 raising overall portfolio to 38 hotels and 9 residences. 28 more hotels and another 2 residences are in the pipeline to be opened over the next 5 years, so this is a growing group.

Bottom Line

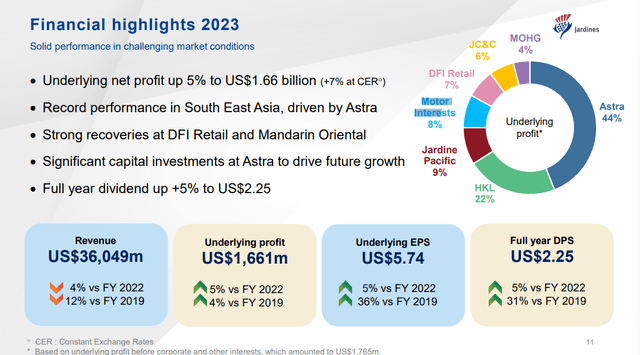

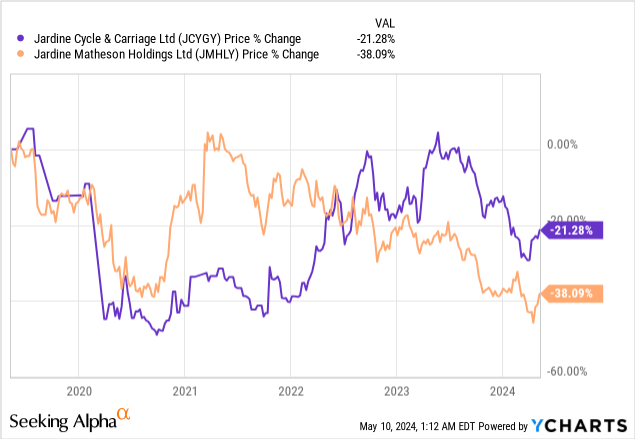

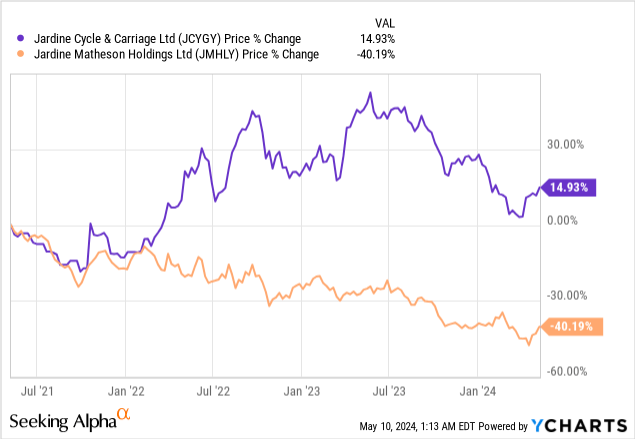

Let’s start getting to the value case. We note the trading value of Jardine Matheson compared to Jardine Cycle & Carriage Limited, which is the publicly listed controlled holding containing Astra that focuses on the Indonesian market, discussed above. C&C has performed a lot better than Jardine Matheson on the 5Y and 3Y horizons. C&C’s value accounts for about half of JM’s market cap.

The divergence can be explained by one primary thing, which is the China factor. Both the Chinese segments, as discussed above, and C&C segments are achieving overall profit growth, particularly segments levered to China within JM due to the reopening, which just means the uninvestability of China has been the primary factor driving very different returns in the stocks particularly since the onset of geopolitical questions about China in 2022. Indeed, JM used to trade as a premium stock with P/Bs at around 0.7x in 2020, now at less than 0.4x, while C&C is above its 202 level of 0.85x at 0.98x now.

Clearly, Jardine Matheson Holdings Limited stock is extremely cheap, trading at less than a 7x P/E, with a strong, almost 5% dividend yield as well, undergirded by solid and profitable businesses and an elite real estate portfolio in Hong Kong. Its income is even solidly growing on the back of the reopening in China, and the end of COVID-zero, which has been the primary earnings driver for the company. The factor at play isn’t operational, it’s today with the foundational problem of whether Chinese, now fully including Hong Kong, assets are actually securities or not.

We think that there are possible upsides at this point in Chinese equities, which have come close to all-time 2005 nadirs in P/B. China’s economic nationalism can only go so far before being suicidal, evidenced by the consequences of retaliatory economic nationalism by the West with things like the CHIPS Act, and that the line that the CCP seems very unwilling to cross is appropriation. Sentiment is close to lows at this point, and we think that people will become more comfortable with the risks that tangible, income generating, but Chinese linked assets have to offer over time.

Jardine Matheson’s P/B has shrunk as its main non-Chinese business P/B has stayed relatively solid. It also has a history of being valued with a premium P/B. C&C is around 50% of JM’s overall underlying operating profit. That means that thinking in terms of crudely blended average P/Bs, the Chinese (that is to say ex-C&C) assets within JM have fallen to extremely low levels, much lower than the overall 0.4x which is already extremely low.

You could say that the Chinese assets have received a 75% discount to their P/Bs, while the denominators grow on continued profitability. The CSI 300 hasn’t even declined more than 50% from 2021 highs. Which is probably one of the harshest discounts in Chinese markets. Any recovery in confidence by the major allocators in China would have a massive impact on JM, as it also continues to generate growth and income.

There are, of course, risks. An intensification of the market rifts could come with China invading Taiwan, which might just be an inevitability, as the West tries to re-station Taiwanese strategic assets closer to home. There are other ways in which the increasing multipolarity of the world order could trigger moves that could intensify fears about the security of assets ultimately held in China. At least many of JM’s businesses are outside of China, and its stocks are listed in Singapore.

Another way of thinking about valuation is that outside of C&C, the assets are primarily properties through Hongkong Land and retail/automotive. Roughly 50% of the value of JM’s stock can be accounted for by C&C, which is also around 50% of underlying profit. That means that property and retail assets, classes of assets that typically have fair yield of around 5-7%, are yielding at closer to 20%, which the JM’s earnings yield (reciprocal of P/E). However, while it is only a directional case, that C&C, a major part of the JM business, is performing well while the JM stock is performing badly just means that the assets underlying JM outside of C&C might deserve some additional attention, especially as the C&C business itself is also nice to own.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.